Small business owners, here’s something you might not know: insurance is your unsung hero. Picture this—one unfortunate event, a slip-and-fall, or perhaps an unexpected fire, and suddenly, everything you’ve worked for could be at risk. Comprehensive insurance isn’t just a luxury; it’s a necessity, a safety net protecting your business from life’s unpredictable curveballs.

Whether you’re running a quaint coffee shop or a burgeoning tech startup, understanding the nuances of small business insurance can make or break your operation. We’ll delve into various insurance types tailored for small businesses, compare them with personal insurance, and highlight the critical safeguards your enterprise needs. Welcome to the ultimate guide on securing peace of mind for your small business!

Understanding Small Business Insurance

Did you know that 40% of small businesses never reopen after a disaster? Insurance is your lifeline!

Here’s why: Small business insurance protects you from the unexpected financial setbacks that could easily sink your business. It covers everything from property damage to liability claims. Without it, you’re just one accident away from massive unplanned expenses.

The Importance of Insurance for Small Businesses

Small businesses face a range of risks daily. A sudden lawsuit or a natural disaster can spell financial ruin. Insurance acts as a safety net, helping you absorb these shocks and keep your business running smooth. It’s crucial to understand that insurance isn’t just an expense—it’s an investment in peace of mind.

Types of Small Business Insurance Policies

There’s a wide variety of policies tailored to different needs. Here’s the deal: Whether you need general liability, worker’s compensation, or professional liability insurance, each policy serves its unique purpose.

- General Liability Insurance: Covers bodily injury and property damage.

- Professional Liability Insurance: Protects against negligence claims.

- Business Interruption Insurance: Covers loss of income due to unforeseen disasters.

Small Business Insurance vs. Personal Insurance

Think personal insurance is enough? Think again! Business insurance safeguards your company’s assets and employees, while personal insurance typically covers personal assets. These are two different beasts.

| Small Business Insurance | Personal Insurance |

|---|---|

| Covers employees and business property | Covers personal property and personal liabilities |

| Includes liability for professional services | Excludes business-related liabilities |

Examples of Businesses Needing Specific Insurance Types

Different businesses have different insurance needs. For example, a tech startup may need a strong data breach protection, while a restaurant might prioritize food safety insurance. Pro Tip: “Tailor your insurance package to match your industry’s unique risks.”

If you’re a consultant, don’t skip on professional liability insurance—it could save thousands in legal fees.

Types of Coverages

Ever thought about the types of insurance your business actually needs? It’s not just about ticking boxes. It’s about safeguarding your livelihood from unexpected disasters.

It turns out, over 40% of small businesses never reopen after a disaster. But the right insurance coverage can ensure you’re not part of that statistic. Here’s the deal: understanding the various insurance coverages available can be the key to business survival.

Main Coverages Under Small Business Insurance

Let’s break down the key types of insurance coverage every small business owner should consider.

| Type | Description | Applicability | Example |

|---|---|---|---|

| General Liability Insurance | Covers third-party claims of bodily injury, property damage, and personal injury. | Essential for all businesses, regardless of size or industry. | A customer slips in your store and breaks their arm. |

| Professional Liability Insurance | Protects against claims of negligence or mistakes in professional services provided. | Ideal for service-based industries such as consultants and accountants. | An accountant makes an error on a client’s tax return. |

| Commercial Property Insurance | Covers damage to physical assets like buildings and inventory. | Important for businesses owning or leasing property. | A fire damages your retail store. |

| Workers’ Compensation Insurance | Provides benefits to employees for work-related injuries or illnesses. | Mandatory in most states for businesses with employees. | An employee is injured using machinery. |

Critical Coverages for High-Risk Industries

If you’re in a high-risk industry, the stakes are even higher. Construction or manufacturing businesses, for instance, can’t afford to skip comprehensive coverage.

Failing to include adequate insurance can lead to massive financial pitfalls. Picture this: a construction worker gets injured, and you haven’t got the coverage. You’re looking at potentially huge liabilities.

The Safety Net of Comprehensive Coverage

So, what does comprehensive coverage really mean? It’s not just about fulfilling legal obligations. It’s about providing a safety net for every aspect of your business.

Comprehensive coverage helps protect against unexpected events like fires, lawsuits, or even cyber-attacks. Imagine being sued for a breach of contract—with proper coverage, you’re not covering legal fees out of pocket.

Pro Tip: “Never underestimate the power of a well-rounded insurance policy. It’s your best bet against the unpredictable.”

Financial Implications of Lacking Necessary Coverages

The financial implications of not having the right coverage can be staggering. A single unforeseen event can drain your resources faster than you can say “insurance.”

Without proper insurance, businesses might face total shutdown. Litigation costs alone can run into hundreds of thousands of dollars. Here’s the harsh reality: it’s not just about risk—it’s about survival.

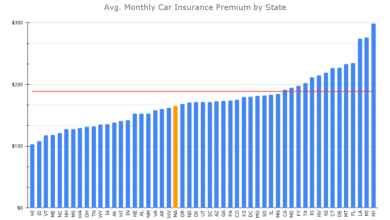

Factors Influencing Insurance Costs

Ever wondered why your small business insurance premiums are through the roof? It’s not just random chance. There are specific factors that determine these costs.

Understanding these variables can help you save a ton of money. Let’s dive into what influences your insurance rates the most.

Key Variables Affecting Insurance Costs

Your insurance premiums aren’t set in stone. In fact, they vary based on several key factors. Things like your industry, the years you’ve been in business, and your credit score all play a huge role.

For instance, high-risk industries like construction tend to have higher premiums compared to a low-risk profession such as consulting. Additionally, if you’ve had a lot of claims in the past, you can expect to pay more.

How Business Size and Location Impact Costs

Believe it or not, your business’s size and location have a massive impact on your insurance costs. Larger businesses with more employees are seen as higher risk and usually pay more.

The location of your business matters too. If you’re in a flood zone or an area prone to natural disasters, expect to shell out more for coverage.

Saving Money: Methods to Lower Your Insurance Costs

Who doesn’t want to save money? Here are some tried-and-true tips for slashing your insurance premiums:

- Bundle your policies to get a multi-policy discount.

- Improve your business’s security to qualify for lower rates.

- Increase your deductible to lower your premium.

- Review your policy annually to ensure you’re not over-insured.

Pro Tip: Investing in risk management can drastically lower your insurance costs in the long term.

Checklist for Evaluating Insurance Costs vs. Benefits

Don’t pay for insurance blindly. Here’s a handy checklist to ensure you’re getting your money’s worth:

- Determine your coverage needs based on your business type.

- Compare premiums from at least three different insurers.

- Evaluate the insurer’s reputation and claims process.

- Check for any hidden fees or exclusions.

Here’s the deal: the right insurance policy should be a balance between cost and coverage. Make sure you’re protected where it counts.

Selecting the Right Insurance Provider

Think all insurance providers are created equal? Think again. This choice can make or break your small business’s financial health. Choosing wisely isn’t just an option; it’s a necessity.

The right insurance provider shields you from the unexpected. A bad one? Well, that could be a costly mistake. Let’s dive into what you need to consider when making this crucial decision.

Key Criteria for a Reliable Insurance Provider

When selecting an insurance provider, focus on the essentials. Licensing and accreditation are non-negotiable. Verify they are authorized to operate in your state. Next, consider their financial stability. Utilize ratings from agencies like A.M. Best to ensure they can pay out claims when disaster strikes. Finally, don’t ignore customer service. Quick, reliable response times can save you stress and money down the line.

Assessing Provider Reputations and Reviews

You wouldn’t hire an employee without checking their background. Do the same with your insurance provider. Start by scouring online reviews and forums where fellow business owners congregate. Don’t just stop at anecdotal feedback. Consult professional reviews—these often give a more comprehensive picture.

Pro Tip: “Customer reviews highlight real-world experiences that marketing materials hide.”

Comparing Local vs. National Insurance Providers

Is bigger always better? Not always. Review the differences between local and national providers:

| Local Providers | National Providers |

|---|---|

| Typically more tailored to regional risks and needs | Offer broad coverage options, often with more resources |

| Establish personal connections leading to customized advice | More standardized processes, sometimes leading to bureaucracy |

| Faster, more flexible response times | Wider network and availability across states |

Negotiating Favorable Terms with Providers

You want the best terms, right? It comes down to effective negotiation. Research similar businesses and understand current market rates to strengthen your position. Don’t hesitate to leverage competitive quotes from other providers. They want your business, so use this to your advantage to extract better premiums and terms.

Finally, build a relationship with your chosen provider. A good rapport means they’re more likely to be flexible and accommodating when you need it the most.

Pro Tip: “Negotiating is not about being aggressive; it’s about being informed and assertive.”

Real-Life Small Business Insurance Claims

Ever wondered what actually happens when a small business makes an insurance claim? Here’s a peek into the real world of business insurance claims.

Understanding the ins and outs of how businesses handle insurance claims can save you both time and money. Let’s look at some real-world cases and what you can learn from them.

Learning from Actual Claims Experiences

Insurance is not just a safety net; it’s a lifeline in crisis. Still, many businesses stumble during claims.

Case Study: A small bakery faced a fire accident, which resulted in $100,000 in damages. Thanks to their comprehensive insurance policy, they were covered for fire damage and lost income during the repair period.

From this, we understand the importance of having the right types of coverage. But here’s the deal: many businesses don’t realize what their policies actually cover until it’s too late.

Common Pitfalls During the Claims Process

When it comes to filing claims, things can go south fast. So how can you avoid common pitfalls?

- Not documenting damage thoroughly

- Missing important deadlines

- Failing to understand policy details

To circumvent these issues, back everything up with documentation. Take pictures, keep receipts, and note every detail. Pro Tip: Always keep a digital copy of your policy handy to quickly verify coverage when disaster strikes.

The Critical Role of Insurance Brokers

Let’s talk about brokers. These professionals are your guides through insurance mazes.

When claims become tangled, insurance brokers act as mediators between you and the insurer. They ensure smoother communication and help expedite claim resolutions.

Case Study: A tech startup suffered a major cyber attack. Initially denied coverage, the firm’s insurance broker intervened, presenting clear evidence of coverage for cyber incidents, leading to a successful claim.

Involving an experienced broker from the get-go can make a world of difference. They’re not just selling policies—they’re advocating for your business when you need it most.

Future Trends in Small Business Insurance

Did you know that 40% of small businesses are underinsured? As the landscape evolves, staying ahead of the curve is crucial for protecting your business.

The world of small business insurance is changing at lightning speed. New risks and technologies are emerging, creating fresh opportunities—and challenges—for business owners. Let’s dive into the future trends you need to be aware of.

Emerging Insurance Products for Small Businesses

Today, small businesses need more than just basic liability coverage. We’re seeing a surge in cyber insurance policies designed to protect against data breaches. With cybercrime expected to cost the world $10.5 trillion annually by 2025, can you afford to skip this? PLUS, business interruption insurance is getting an upgrade, now covering disruptions caused by pandemics or natural disasters.

Pro Tip: Don’t just settle for general liability. Customize your plan with niche policies that target your specific vulnerabilities.

Technological Advancements Affecting the Insurance Industry

You know technology is transforming everything. But here’s the deal: AI and machine learning are now revolutionizing how insurers assess risk and claim processing. This means faster, more accurate premiums tailored specifically to your business needs. And guess what? Blockchain is stepping in to increase transparency and decrease fraud—a win-win situation.

The Impact of Global Events on Insurance Policies

Global dynamics can no longer be ignored. Events like COVID-19 and climate change have fundamentally altered what businesses need from insurance providers. Suddenly, pandemic insurance is more than a buzzword; it’s a necessity. On top of that, environmental liabilities are making eco-insurance a must-have, particularly for businesses looking to go green.

Evolving Needs for Insurance Coverage in the Modern Marketplace

The gig economy is booming, and your insurance should reflect that growth. Freelancers and contractors are increasingly demanding personalized coverage options. PLUS, as remote work becomes the new norm, home-based business policies are rising in popularity, ensuring the workspace—and what’s inside it—is fully protected.

As we move forward, keep an eye on these trends. They might just dictate your next insurance policy decision!

Conclusion

Securing your small business with the right insurance isn’t merely a checkbox to be marked off. It’s about strategically safeguarding your vision and livelihood. With the right coverage, you’re not just insuring; you’re investing in security and sustainability. As we wrap up, remember, the right policy can mean the difference between thriving and just surviving when unexpected challenges arise. Here’s to making informed decisions and building a resilient business future!

Answers to Common Questions

What is the importance of small business insurance?

Insurance protects your business from financial losses due to accidents, lawsuits, and natural disasters, ensuring continuity.

What are the different types of small business insurance policies?

They include General Liability, Professional Liability, Commercial Property Insurance, Workers’ Compensation, and more.

How does small business insurance differ from personal insurance?

Small business insurance covers risks associated with business operations, while personal insurance covers individual-related risks.

Which small businesses need specific insurance types?

Examples include tech startups requiring cyber liability insurance and restaurants needing product liability coverage.

How can small businesses lower their insurance costs?

By bundling policies, improving workplace safety, and choosing higher deductibles.